Even though Apple was founded in 1976 and went public in 1980, it wasn’t until many years later that the stock really exploded. If you had made an investment in Apple on October 31, 2001, you would now be sitting on a gain of 38,854%. That’s without including dividends or reinvestment.

So why October 31, 2001?

That’s the day that Apple released the first iPod. This would lead the way for the company to completely shake up the world of consumer electronics. It could be argued that the release of this now antiquated piece of technology was more important than the company’s position in personal computers.

If you had waited until the first iPhone release on June 29, 2007 to invest in Apple, you’d still be sitting on a solid return of 2,702%. Or how about when the first iPad was introduced in April 2010? That’d be a gain of 1,209%.

Even if you’re an avid Android user, you can’t argue against the iconic status of the iPhone and the iPad.

But really this is just one example of the incredible businesses that have been built over the last 20 years. Apple had its hero product with the iPod. Complete with Apple music which launched eight months earlier, it literally changed the landscape of listening to music on the go.

This first iPod only held 1,000 songs. It wasn’t a replacement for your CD collection, but it was for your Walkman. As technology continued to advance and storage began to get more affordable, that capacity could increase. Apple could continue to innovate and build more products using that same technology and infrastructure.

This is just one example. The evolution of technology as a whole has touched almost every aspect of our lives. Apple with music and phones. Amazon has changed the way that we shop for everything from groceries to electronics. Netflix changed the way that we rented movies, and has taken that further into streaming.

The company that I have for you today is taking on one of the oldest and stodgiest industries around.

The story of this big shake-up also dates back to the early 2002, when the first real fintech went public.

Fintech is essentially financial technology. It’s quite a broad term and refers to the integration of technology into the financial realm. This could mean anything from digital payments to processing alternative financing or even using technology to manage personal finance.

One great example is PayPal, the company we referenced above. It was one of the first public fintech company and is currently one of the biggest. Although, it’s been branching out into concepts such as bitcoin, its main realm is digital payments. You can send money to the largest retailers in the world or to your neighbor all with a few clicks.

But, as I mentioned above, the term fintech has a wide scope. And now, more than ever, we’re seeing companies turn attention to this sector.

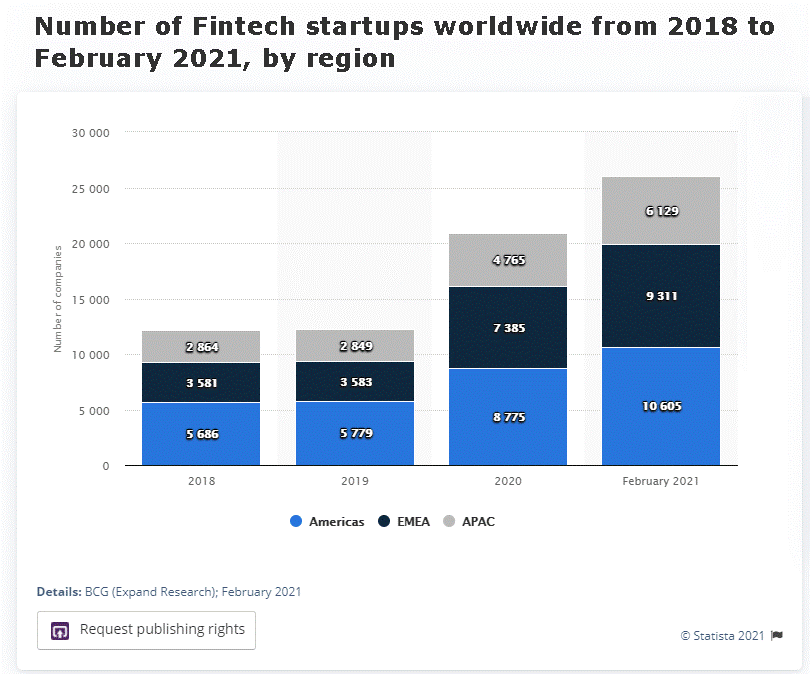

Take a look at the chart below:

We are at a point in time where the number of fintech startups worldwide is about to explode. Technology has changed the way that we listen to music, the way that we watch television and even the way that we shop. Now it’s time to really unlock the potential of technology in the way that we handle monetary transactions and handle our personal finances.

It’s about time.

The First Bank of the United States was opened in 1791. It was tasked to handle debt from the Revolutionary War, create a standard form of currency and raise money for the new government. Sure, banks have adapted with the changing times and adopted minimal technology.

But, since 2012 coming out of the Great Financial Crisis there has been a stagnation. Large financial institutions offer the most products and the same standard accounts. Even if you can go to your local bank or credit union, but you’re going to see the same old products. You’ve got checking accounts, savings accounts, certificates of deposits and lending.

The 2019 FDIC survey found that nearly 95% of U.S. households were banked, meaning had a bank or credit union account. This is the highest number and percentage of households with bank accounts since the survey was first conducted in 2009.

The real question here is are these consumers satisfied with their accounts or do they simply have them because the world has deemed that they need a bank account? Is there anything else to choose from?

As we transitioned toward a more digital landscape in all aspects of our society and economy, we are seeing a trend of neobanks. These are financial technology firms that offer internet-only financial services and do not have physical branches.

Neobanks are working to disrupt the stale product line that consumers are faced with when walking into a bank. Neobanks are the MP3 players of 2021. Some will fall to the wayside like the Dell Jukebox and others will pave the way for the future like the iPod.

Social Finance Inc. or SoFi has its sights set on becoming a one-stop shop of neobanks. Whether you need a loan, wants a place to keep your money or want to start investing in stocks, ETFs, or cryptocurrencies, SoFi can help. There are tens of thousands of financial institutions, but SoFi believes that they can do it better.

Even though the company offers many of the same products and services as a traditional bank or credit union, SoFi is not a bank. Instead, the company is a registered broker/dealer, which means its still held to high regulatory and compliance standards. This differentiation allows for it to offer consumers different ways to manage their money.

The company’s SoFi Money account is equivalent to Apple’s iPhone. It isn’t the company’s first product, but it’s a culmination of the technology and could be view as essential to any person of any age. Upon first glance it looks extremely similar to a checking account.

The customer has a linked debit card and can even get paper checks associated with the account. You can deposit checks, pay bills, and even set up auto bill pay. You can set up your direct deposit and access online “banking” services through an app on your smartphone. The money in it is even FDIC insured up to $1.5 million.

SoFi Money is a cash management account. It is based on the SoFi philosophy that you should

This cash management account is essentially a brokerage account. It has no fees and can earn 0.25% APY. Plus, SoFi allows for easy P2P money transfers.

Once customers have their money into this account, they can easily move into the SoFi Invest product. Not only can customers buy stocks, but they can also buy cryptocurrencies right there as well. But SoFi takes its investing options one step further.

First, it offers its own ETFs. Right now, there are five of them, but we’re sure once these prove popular the company will continue to expand. Second, SoFi allows for fractional share investing. This means that instead of committing to a certain number of shares, investors can commit to a specific dollar amount. This makes some of the larger tech names, including Apple more accessible to investors.

Finally, it allows for eligible members to participate in upcoming IPOs before they trade on an exchange. And you can be eligible with as little as $3,000.

SoFi wants to make it so that you not only want to give them your money that’s earmarked “checking account”, but that you continue to manage your money through their multiple products.

In fact, the company started out as a student loan refinance business. Founded in 2011, it was founded by Stanford business school students. It used an alumni-funded model to connect recent grads with alumni in their community. Shorty after, it became the first company to refinance federal and private student loans.

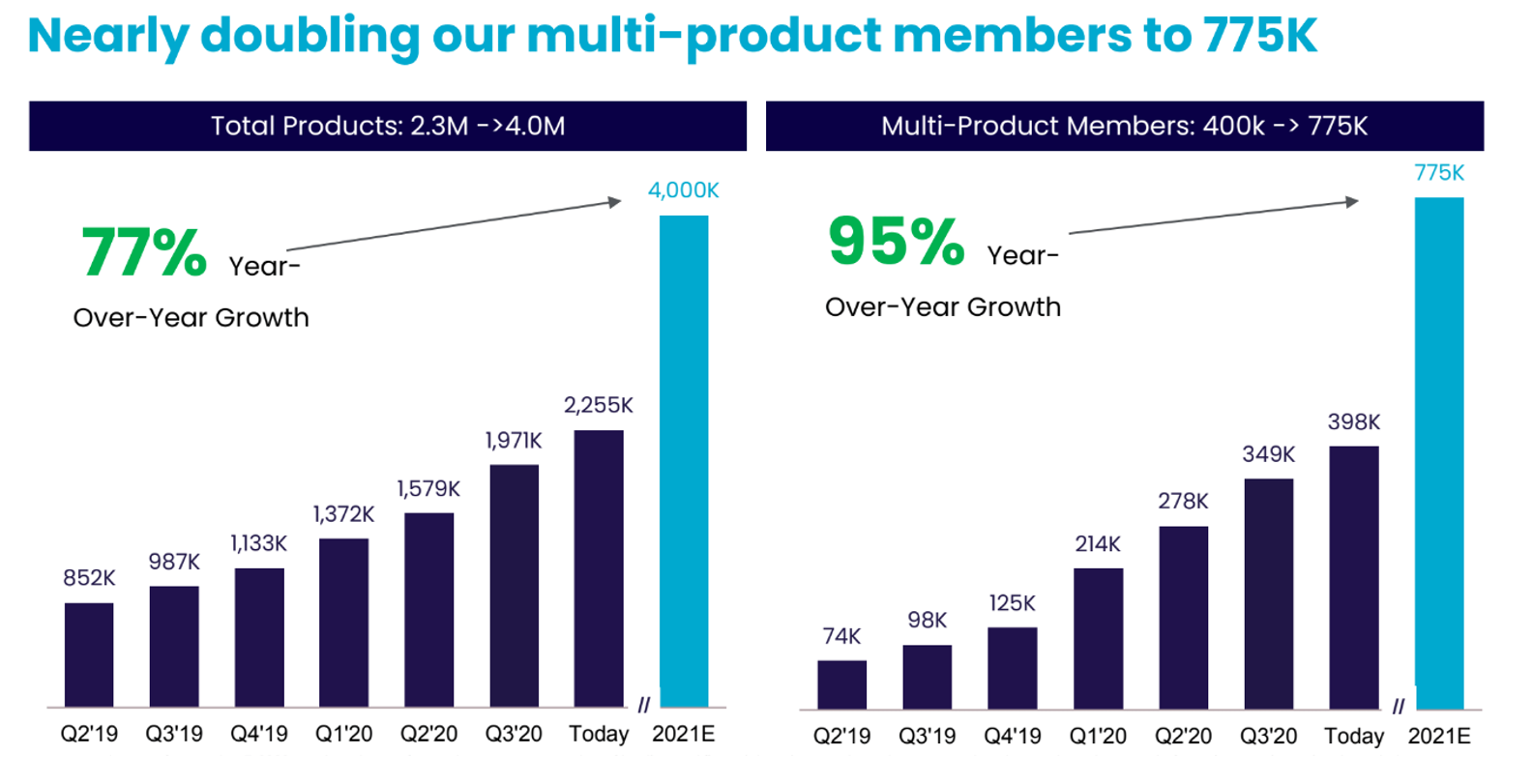

Now with nearly 2,000,000 members, the company is embracing the true meaning of cross-sell and up-sell. But since there are no physical locations and bankers with quotas, you’ll find it’s less selling and instead simply offering as many products as possible. The company even has SoFi Relay which is a credit score monitoring and money tracking product. And members can shop for all their insurance needs using SoFi Protect.

This breadth of products allows for easy attraction of new customers who can then be cross-sold, and the process just keeps repeating itself. This will make it easy for the company to hit its 2025 revenue prediction of over $3.5 billion. And this story is certainly why investors are taking note before you can even technically buy shares.

I’m not here to predict that this company will be the next PayPal. It doesn’t just want a slice of the pie like PayPal does with payments…SoFi wants the whole pie.

The company recites that 59% of people have increased their fintech app usages as offline management of finances have fallen. And that 87% of consumers say they won’t go back.

Now, they don’t really say where these number come from or the parameters of the survey, but the argument for the change in consumer behavior is there.

This is just one more example of how COVID-19 accelerated a trend. We were already moving towards digital banking and touchless payments. But then all of a sudden, we found that we no longer had access to branches, and tellers and bankers. So why not move to a company that’s optimized for this digital landscape.

I think that investors clearly see this trend and are going to rush into this stock once it hits the exchange, despite the fact that it’s not yet profitable.

It has the products that are shaking up an old industry. On top of that it has an incredibly diverse and experience management team that comes from some of the biggest names in tech. These guys and gals have been at Twitter, Intuit, Uber, Amazon, Citi. They have seen the change in each respective landscape and are ready to bring SoFi to that same level.

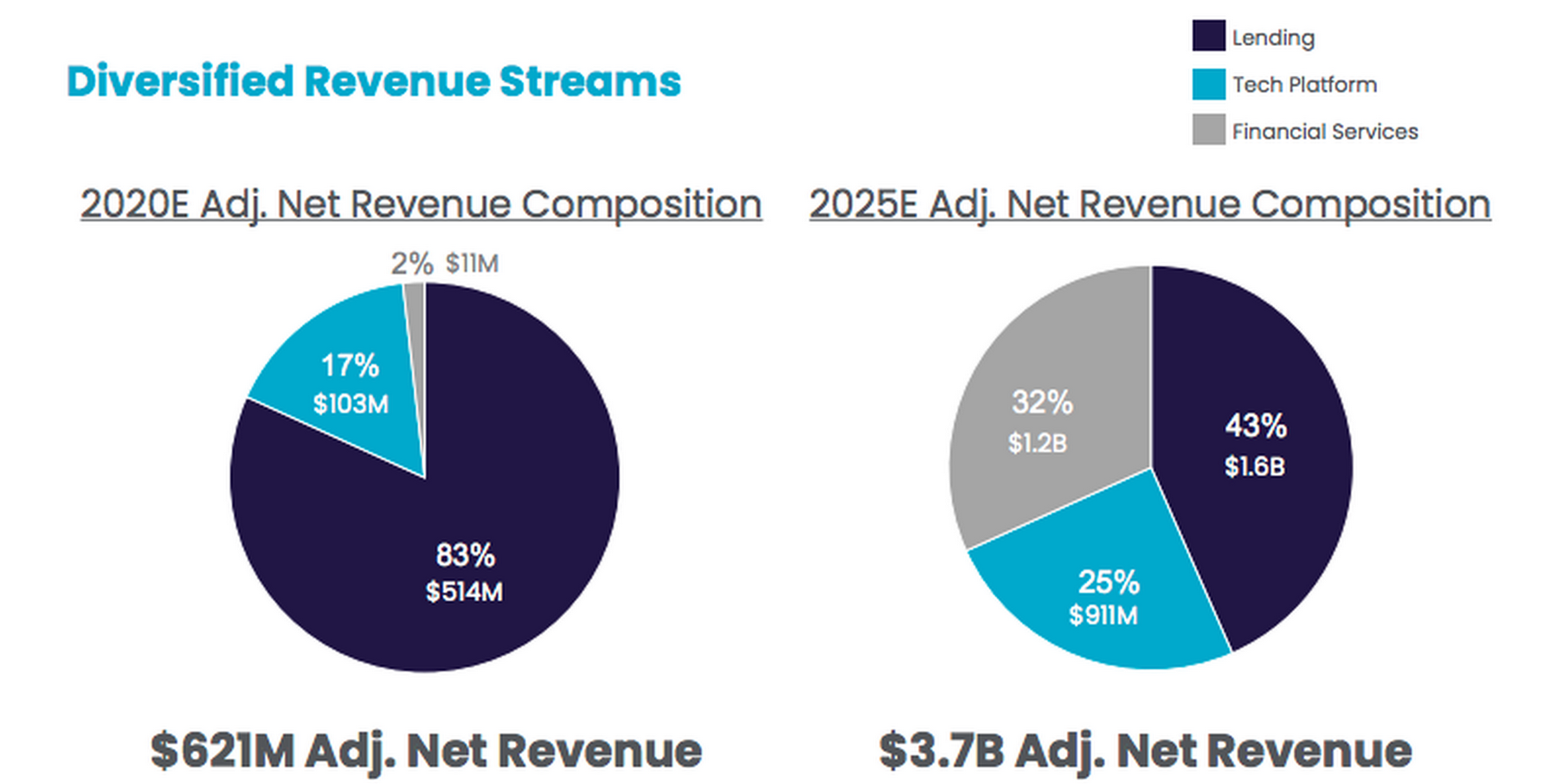

The company has suggested it expects to see adjusted net revenue of $980 million over the course of 2021. And expects that to reach $3.6 billion by 2025.

On the surface a prediction of 58% growth compared to the $621 million net revenue for 2020 may seem lofty. But the company saw an increase of 89% from 2018 to 2019, and 38% growth in 2020 despite the impacts of COVID-19.

It should only be a matter of time now before shareholders will be able to get their hands of SOFI shares. The company has announced that it will be combining with the SPAC Social Capital Hedosophia Holdings Corp (NYSE: IPOE).

Investors had expected this transaction to close during the first quarter of 2021. But clearly there’s a different timeline in play which hasn’t been updated to investors.

I could speculate that SoFi might want to finalize its acquisition of Golden Pacific Bancorp first, but it could be any number of hold-ups. Even still, I think that we will see this merger close sooner rather than later.

And this skilled management team isn’t going to take any time at all to continue to grow the company and change the landscape of banking as we know it.

Action to take: Buy shares of Social Capital Hedosophia Holdings Corp (NYSE: IPOE).

Until next time.

Sincerely,

Joshua M. Belanger