Volume #1 Issue #9

In This Issue…

The Great Consolidation Is Upon Us

There’s a gap in the economy. It’s not new, but its widening at an accelerated pace. And it means that some companies are going to soar, and some companies will cease to exist. A great consolidation is right around the corner as we see those caught in this trend try and figure out a way to survive.

Expanding and Moving into the Future

Instead of sitting around and waiting to become irrelevant, this company is always looking to change and grow with the technology. That includes keeping an eye out for any acquisitions that would fit to serve its clients.

Earnings Season Ramps Up for Our Holdings

We’ve got a lot of earnings updates for the positions in our open portfolio…some good and some not so great. But, either way, we take a minute to break down the highlights and see what they mean our positions.

In 2013, Brad Stone wrote a book called The Everything Store. It is the story of an ambitious and relentless man who is determined to create and online store that will someday be “everything to everyone.”

No one will dispute that Jeff Bezos is working closer and closer to that goal every day.

What started as an online bookstore in 1994 is now an electronic commerce and cloud computing giant.

It’s now one of the big four of tech.

Its secret?

It has acquired or invested in over 128 companies. And many of those have been after 2005 when it started heavily focusing on digital retailers and media websites. In 2011, Amazon started going after technology startups.

The result was the Amazon Echo and the birth of its Amazon Web Services. Even though its largest purchase of Whole Foods Market in 2017 was clearly a winner, it’s the tech that’s going to keep the company moving into the future.

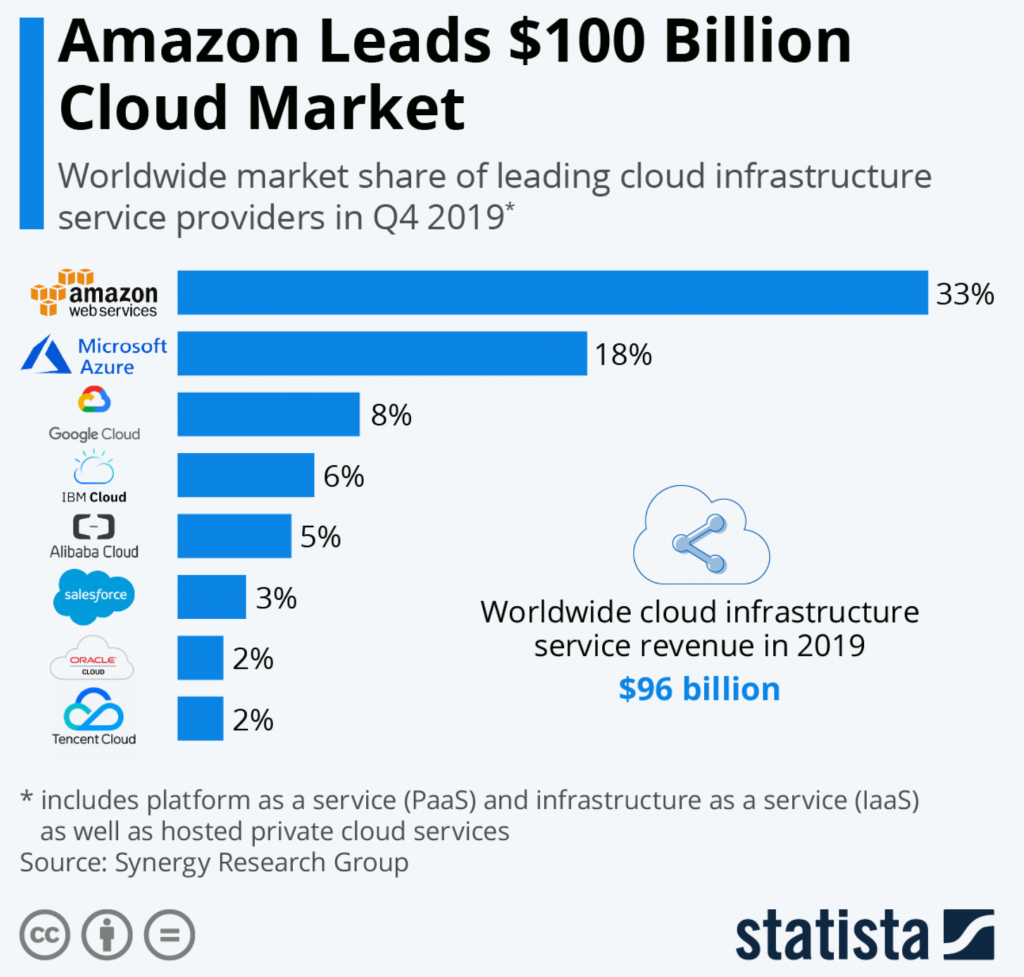

Amazon Web Services is the leader in the cloud infrastructure market…and not by just a little bit.

But this wasn’t because the company created some brilliant tech from scratch.

Management was patient with making the right purchases at the right time. By combining a little from this company and a little from that company…it took the lead.

The recent pandemic has accelerated how quickly and efficiently companies optimize teams remotely through current technology.

And Amazon’s solution is to keep making strategic moves to outreach the competitors.

Right now, it’s eyeing up a minority interest in Rackspace. Amazon already partners with Rackspace, but now it wants a piece.

We’re not surprised in the slightest by these discussions. Rackspace is a company that guides organizations through the whole process of setting up and managing its cloud. It focuses on optimization, security, and data modernization. Essentially it helps organizations step into the future.

To do that effectively, Rackspace has partnerships with all the could giants. This allows it to recommend the right services for the right problem. You can quickly start to put the pieces together of why Amazon wants this in its arsenal.

And it’s not just Amazon that’s continuing to look for the right companies to add to its portfolio.

Uber bought Postmates for $2.65 billion. Facebook bought Giphy for $400 million., Zoom acquired encryption specialist Keybase…Those are just a few examples from 2020 so far.

And these are just some from the headlines. There will be even more taking place amongst companies that you’ve never even heard of as they try and stay afloat in the current economic climate.

The Great Consolidation Is Upon Us

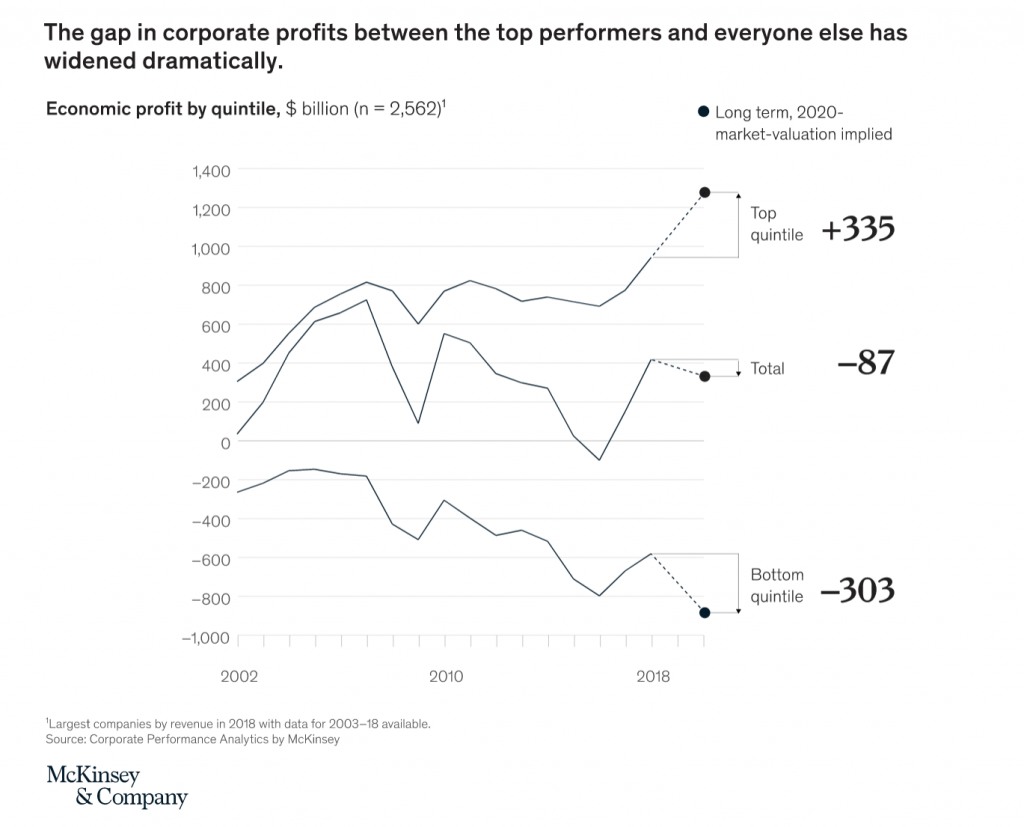

There is an undeniable gap in the market.

I’m talking about the profits of the top performers in a sector verses the bottom performers in a sector. This isn’t anything new, but it’s getting worse as leaders find their way to succeed and the bottom performers have been rushed into bankruptcy.

Check out this chart from McKinsey & Company.

The gap was already there and getting bigger, but the Coronavirus has accelerated its pace.

The evidence is all around use. Restaurants and retail are clear tangible examples.

Dominos, McDonalds and Wing Stop are all flourishing. Why? All three have simple menus and were already utilizing online ordering. On the flip side Bar Louie, California Pizza Kitchen and Toojay’s have already filed for bankruptcy.

The top performers will keep seeing the profits and the bottom performers are shuttering up forever.

This is also happening in the technology space.

The leaders are succeeding... while the losers are heading down at a more rapid clip. But there is an important difference in the sectors. McDonald’s has no interest buying a washed-up Bar Louie location.

In other sectors such as energy, mining and technology we’re going to see what we call a great consolidation. That’s right, we’re going to see an increase in acquisitions and mergers.

The companies in good financial standing will pick up the not so successful for pennies on the dollar. And the companies treading water in the middle will look for opportunities to merge with others in that position. Tech will be leveraged and combined so these companies can innovate and compete.

This will be especially prevalent in the two categories that we like to talk so much about: software and internet.

Last month, we pointed out that the future is looking toward software as a service (SaaS). And it’s even more than that. Companies are moving towards network as a service (NaaS). This allows for entire networks to exist with specialized hardware sitting in expensive office space.

In 2019 alone, over $400 billion was spent on enterprise software…and it’s expected to keep growing at 10%.

The companies that supply the best enterprise software solutions will be the real winners after the Coronavirus. Employees are going to be accustomed to working from home at least part time. It’s a genie that won’t be able to be put back into the bottle.

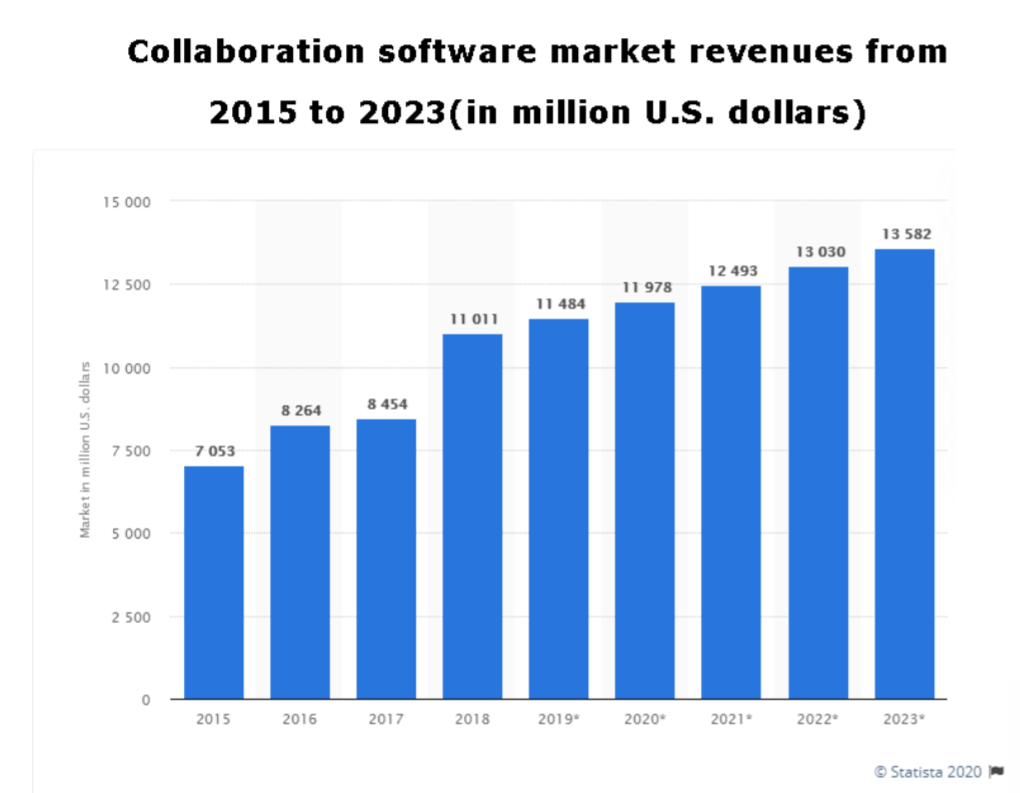

The company that we’re recommending today is part of a segment of enterprise software that has been growing steadily since 2015…but even more in demand today…collaboration software.

Keeping Projects Moving in an Orderly Fashion

The 2020 collaboration software market revenue was expected to be nearly $12 million. That was before the impact of the Coronavirus.

According to a survey of global business professionals conducted by Harvard Business Review Analytic Services, three-quarters of respondents agreed that the pandemic revealed major gaps in their internal technology strategy. Ninety-three percent agreed it’s necessary to provide teams with the software and tools needed to produce successful work.

That means that mangers everywhere will be looking for services from the company that we have for you today.

Smartsheet (NYSE: SMAR) is a leading cloud-based project management solution. Its products allow teams and organizations to plan, capture, manage, automate, and report in a way that results in more efficient processes.

The software uses a user-friendly tabular interface that allows for assigning tasks, tracking progress, managing calendars and sharing documents.

And since it’s based in the cloud, it can be used for collaboration not just across the team, but across an entire division or even between organizations. And as we’ve stressed multiple times, this will become even more important as employees find themselves working remote at least part time for the infinite future.

“Smartsheet has become an increasingly mission-critical platform for enterprises seeking to enable a dynamic workforce; a workforce capable of working from anywhere, adapting to rapidly changing conditions and staying deeply connected to their individual work and mission of their teams, no matter the circumstance,” explains Mark Mader, president and CEO of Smartsheet.

Smartsheet has over 97,000 customers including over 75% of the companies in the Fortune 500.

It is so attractive to all these customers because it structures projects in a different way. Traditional project management tools focus more on the schedule and breaking projects into individual tasks. Smartsheet allows for the focus to be on the collaborative aspects of the project. All while letting the team quickly see the progress.

Unlike most traditional spreadsheets or task apps, the platform allows for switching between visualizations of the same data. This supports collaboration between different departments and teams, who can them access data in the way best for them.

It’s all about increasing effectiveness so that their customers can achieve more while wasting less time searching for information.

The Smartsheet suite of products also includes smart automation that relieves the need to manually do things that are repetitive. And there’s smart integration with enables connection to all your company’s other enterprise software.

Customers are very satisfied with their results when they use Smartsheet. How else would the company reach the milestone of being trust by more than 75% of Fortune 500 companies and 90% of Fortune 100 companies?

Sixty-five percent of Smartsheet users see greater cross-team accountability and participation. Fifty-eight percent see fewer unnecessary emails and 44% see fewer data silos across their organization. But that doesn’t mean that is all Smartsheet has to offer.

Expanding and Moving into the Future

It’s true that Smartsheet has a solid customer base and a solid product. So, what can it do next for its customers?

At the end of August, Smartsheet announced it would acquire the digital asset management company Brandfolder for $155 million.

Digital asset management (DAM) is a system that provides a central space for organizations to store organize, find, access and share digital content. Its integrations into Smartsheet will mean that customers will be able to not only manage digital content but see how they fit into different workflows and gauge performance metrics.

The company will give more details on its second quarter earnings call this week. But this is a prime example of the consolidation we’re expecting to see.

The management decided that Smartsheet could be enhanced by the addition of a DAM. They took after Amazon. Instead of reinventing the wheel, they found the technology already out there and once integrated will be one more step ahead.

Earlier this year, Smartsheet announced another interesting project that could bring in more and more customers. It’s announced its Federal Advisory Board which is comprised of former federal government executive from civilian, defense and intelligence agencies.

The company launched a government offering for public sector organization back in 2019, and it’s taking the time to light a fire on that fuse. These organization have also been affected by the Coronavirus…maybe even more so since they couldn’t possibly stay closed forever.

Both projects show the growth potential for Smartsheet and why it’s time to get in right now.

For the quarter ending April 30, the company saw total revenue of $85.5 million. This was up 52% when compared to the previous year.

The number of customers with annualized contract values (ACV) of $5,000 or more grew to 9,576. The number of customers with ACV of $50,000 doubled since the previous year, as did the number of all customers with ACV of $100,000 or more.

The management doesn’t expect results quite that impressive for the second quarter, but it still expects to see revenue growth of 33% when compared to last year.

But lucky for us, shares haven’t factored all this potential in quite yet.

Smartsheet has only been public since May 2018 and over that time share have more than tripled. But if you look at just the last year, investors haven’t run up these shares like they have with other technology companies.

That’s fine with us, we’ll go ahead and get in right now and ride the upward wave.

The company will announce it second quarter earnings this week. This will give more insight into the short term of the company, but in the long run, Smartsheet is a winner.

Action to take: Add shares of Smartsheet Inc. (NYSE: SMAR) to your portfolio.

We noted last month that there were a lot of earnings calls around the corner. Let’s run through the highlights.

Invitae Corp. (NYSE: NVTA) has spent the quarter introducing expanded services and support for the transition to telehealth across all its customers. The management knew that diversifying and adapting was going to be the key to success during the pandemic. During the quarter the company also added 16 new biopharma partnerships for a grand total of 105.

Revenue for the quarter was $46.2 million, which was down 13% when compared to the previous year. Considering the rapid changes in the healthcare industry that’s not too shabby. Obviously as investors we don’t want to see this number continue to slide. But for now, let’s hold onto these shares since we’re up 203% since our entry last year.

Twilio Inc. (NYSE: TWLO) is a leader in cloud communications. Jeff Lawson, co-founder and CEO pointed out that during the pandemic “organizations in nearly every industry are turning to Twilio as they identify new ways to communicate with their customers and stakeholders.”

As of June 30, the company had more than 200,000 active customer accounts. That’s up 24% year-over-year. And that’s being seen in the numbers. Revenue for the quarter was $400.8 million…up 46% over the previous year.

Twilio also announced that it has been selected to power communications for contact tracing initiatives in more than 28 cities, states and universities. We’re up over 200% since we recommended shares last year.

Pinterest, Inc. (NYSE: PINS) is another company benefitting from people having more free time on their hands. Ben Silbermann, CEO and co-founder explains, “This quarter we reached a milestone—more than 400 million people now come to Pinterest every month to get and stay inspired.”

Despite the challenging landscape, Pinterest saw revenue increase 4% year over year. The company still operates at a net loss; however, this quarter was 91% better than the loss of the same quarter last year. The management knows there is still a lot of work to be done, but investors are seeing the improvement.

Shares are up 70% since we first got into this position, and there is still room for growth.

Our leader in data analytics, Alteryx, Inc. (NYSE: AYX) announced decent second quarter earnings as well. Revenue for the quarter was $96.2 million, which was an increase of 17% year over year.

The company added 271 new customers in the second quarter as well as launched numerous new features on the Alteryx APA platform. It also successfully launched its ADAPT program which offers free data analytics training to thousands of workers globally who have been impacted by the pandemic.

Shares are up over 100% since we originally recommended them.

Fastly, Inc. (NYSE: FSLY) is another one of our holds that is benefiting as the pandemic forces businesses to accelerate into the digital age. Revenue was up 62% when compared to the same quarter last year. The company also saw the largest quarterly customer growth since IPO. What’s even better is the company raising its full-year guidance. And if it hits those numbers it will turn into even more money for us. We’re already up over 400% since we got into this position last year.

Veeva Systems Inc (NYSE: VEEV) announced that it saw total revenues for the second quarter of $353,7 million, which was up 33% when compared to the previous year. CFO Tim Cabral pointed out that “Demand for our products and service remains strong as life sciences companies pursue strategic initiatives across R&D and commercial.” We’re up over 200% since we recommended shares last year.

Okta Inc (NASDAQ: OKTA) announced it saw revenue increase 43% when compared to the previous year. It’s CEO and co-founder Todd McKinnon justifies his company right now the same way we would.

He says, “The three mega-trends that have been driving out business for the past several years – the adoption of cloud and hybrid IT, digital transformation and zero trust security – are all being accelerated globally by the current environment.”

Due to the circumstances, the management has raised the outlook for the fiscal year for both revenue and profitability. We’re up over 200% since we originally recommended shares last year.

One company that was hit hard but the pandemic was Gogo Inc (NASDAQ: GOGO). We like this company because its goal is to ring the internet to the sky, so planes fly smarter, airlines perform better, and passengers travel happier.

The company recently announced that it has hit the milestone of 1,000 installs of its AVANCE L5 system, but that’s not enough to offset all the struggles of the quarter. Revenue for the quarter was $96.6 million for a net loss of $86 million.

The decline in air traffic has resulted in furloughs and compensation reductions for the team at Gogo. Our shares are down 4% in that last 6 months, but we’re recommending you hold this position for now. If air traffic continues to pick up and we don’t see another spike in cases, we could see business for Gogo start to pick up again before the end of the year.

Advanced Micro Devices (NASDAQ: AMD) also saw a good quarter. Revenue was $1.93 billion, up 26% when compared to last year. The company is seeing strength in PC, gaming and data center products and expects to see 2020 full year revenue beat 2019 by 32%. We’re up 75% since we added shares to our portfolio earlier this year.

Livongo Health Inc (NASDAQ: LVGO) is one of our favorite holdings…and it’s turning out to be one of our most profitable. At the beginning of August, the company announced that it had entered into a definitive merge agreement with Teledoc Health. Right now, we’re up over 300% on those shares.

At the completion of the merger these shares will no longer exits. So, if you continue to hold your shares each one will be exchanged for 0.5920 share of Teledoc Health and cash consideration of $11.33.

Newmont Corp (NYSE: NEM) of course delivered a solid performance during the second quarter since the price of gold rose steadily through the second quarter. The company sees all in cost of approximately $1,097 per ounce. This increase in price helped offset lower volumes and revenue still increased 5% from the prior year.

Plus, the company announced that it would be paying out a dividend of 25 cents which is in line with its regular payment. This is especially important to note since many companies have decided to suspend or lower their dividends this year. Shares are flat since we got in earlier this year.

Cloudflare Inc (NYSE:NET) announced that for the second quarter its revenue totaled $99.7 million, an increase of 48% when compared to the previous year. The CEO also noted that they added a record number of large customers over the quarter and hired more new team members than any other quarter in history.

Cloudflare is one of our holdings that will be benefitting from the trend acceleration that we’ve been seeing in tech. We’re up 34% since we recommended shares in June.

Mimecast Limited (NASDAQ: MIME) announced its earnings at the beginning of August. Total revenue for the quarter was $115.2 million which was a 12% increase when compared to the same quarter of the previous year.

CEO, Peter Bauer points out that “email is seeing increased usage as employees work from home…Mimecast Email Security 3.0 restores treat in email and enables the business to safely rely on this core system while staying connected to customers and employees.” This is one of the key drivers of the 600 new customers added during the quarter.

We’re up 10% in just the 3 months that we’ve held the stock and we expect to see even more growth as its customer base expands.

Our most recent addition Elastic NV (NYSE: ESTC) also just reported earnings at the end of August. For this first quarter of fiscal year 2021, total revenue was $128.9 million. That was an increase of 44% when compared to the same quarter last year. SaaS revenue was up 86%.

This is a company that will keep seeing revenue increase, because they keep enhancing the security and ease of their products. And investors are taking notice.Shares are up over 16% in the short time that we’ve held them.

Upcoming Earnings Releases

PagerDuty Inc (NYSE: PD) on September 2nd

Mongodb Inc (NASDAQ: MDB) on September 2nd